As filed with the Securities and Exchange Commission on May 22, 2023

Registration No. 333-271177

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

_______________________

to

FORM

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

_______________________

(Exact name of registrant as specified in its charter)

_______________________

| | 6770 | 86-2062844 | ||

| (State or Other Jurisdiction of | (Primary Standard Industrial | (I.R.S. Employer |

214 Brazilian Avenue, Suite 200-J

Palm Beach, FL 33480

Telephone: (561) 805-3588

(Address, including zip code, and telephone number, including area code, of registrant’s principal executive offices)

_______________________

Omeed Malik

c/o Colombier Acquisition Corp.

214 Brazilian Avenue, Suite 200-J

Palm Beach, FL 33480

Telephone: (561) 805-3588

(Name, address, including zip code, and telephone number, including area code, of agent for service)

_______________________

Copies to:

|

Douglas S. Ellenoff, Esq. |

Glenn R. Pollner, Esq. Andrew P. Alin, Esq. Judd Abramson, Esq. 250 Greenwich Street |

|

|

_______________________ |

||

Approximate date of commencement of proposed sale to the public: As soon as practicable after this Registration Statement becomes effective and after all conditions under the Merger Agreement to consummate the proposed merger are satisfied or waived.

If the securities being registered on this Form are being offered in connection with the formation of a holding company and there is compliance with General Instruction G, check the following box: ☐

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering: ☐

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering: ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | ☐ | Accelerated filer | ☐ | |||||

|

| ☒ | Smaller reporting company | | |||||

| Emerging growth company | |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 7(a)(2)(B) of the Securities Act.

If applicable, place an X in the box to designate the appropriate rule provision relied upon in conducting this transaction:

Exchange Act Rule 13e-4(i) (Cross-Border Issuer Tender Offer) ☐

Exchange Act Rule 14d-1(d) (Cross-Border Third-Party Tender Offer) ☐

The Registrant hereby amends this Registration Statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment which specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933, as amended, or until the Registration Statement shall become effective on such date as the Securities and Exchange Commission, acting pursuant to said Section 8(a), may determine.

The information in this preliminary proxy statement/prospectus is not complete and may be changed. These securities may not be issued until the registration statement filed with the Securities and Exchange Commission is effective. This preliminary proxy statement/prospectus is not an offer to sell these securities and does not constitute the solicitation of offers to buy these securities in any jurisdiction where the offer or sale is not permitted.

PRELIMINARY PROXY STATEMENT/PROSPECTUS — SUBJECT TO COMPLETION,

DATED MAY 22, 2023

PROXY STATEMENT FOR SPECIAL MEETING OF STOCKHOLDERS OF

COLOMBIER ACQUISITION CORP.

AND

PROSPECTUS FOR UP TO [__] SHARES OF CLASS A COMMON STOCK AND UP TO [__]

SHARES OF CLASS C COMMON STOCK OF COLOMBIER ACQUISITION CORP.

To the Stockholders of Colombier Acquisition Corp.:

You are cordially invited to attend the special meeting of the stockholders (the “Colombier Special Meeting”) of Colombier Acquisition Corp. (“Colombier”), which will be held at [•] a.m., Eastern Time, on [•], 2023. The Board of Directors of Colombier (the “Colombier Board”) has determined to convene and conduct the Colombier Special Meeting in a virtual meeting format at www.cstproxy.com/[•]. Stockholders will NOT be able to attend the Colombier Special Meeting in-person. The accompanying proxy statement/prospectus includes instructions on how to access the virtual Colombier Special Meeting and how to listen and vote from home or any remote location with internet connectivity. You or your proxy holder will be able to attend and vote at the Colombier Special Meeting by visiting www.cstproxy.com/[•] and using a control number assigned by Continental Stock Transfer & Trust Company and printed on your proxy card. To register and receive access to the Colombier Special Meeting, registered stockholders and beneficial stockholders (those holding shares through a stock brokerage account or by a bank or other holder of record) of Colombier will need to follow the instructions applicable to them provided in the accompanying proxy statement/prospectus.

On February 27, 2023, Colombier entered into an Agreement and Plan of Merger (as it may be amended or supplemented from time to time, the “Merger Agreement”) with PSQ Holdings Inc., a Delaware corporation (“PSQ”), Colombier-Liberty Acquisition, Inc., a Delaware corporation and a wholly-owned subsidiary of Colombier (“Merger Sub”), and Colombier Sponsor, LLC (the “Sponsor”), a Delaware limited liability company, in its capacity as Purchaser Representative (the “Purchaser Representative”), for the purposes set forth in the Merger Agreement (all of the transactions contemplated by the Merger Agreement, including the issuances of securities thereunder, the “Business Combination”). You are being asked to vote on the Business Combination and certain other related matters.

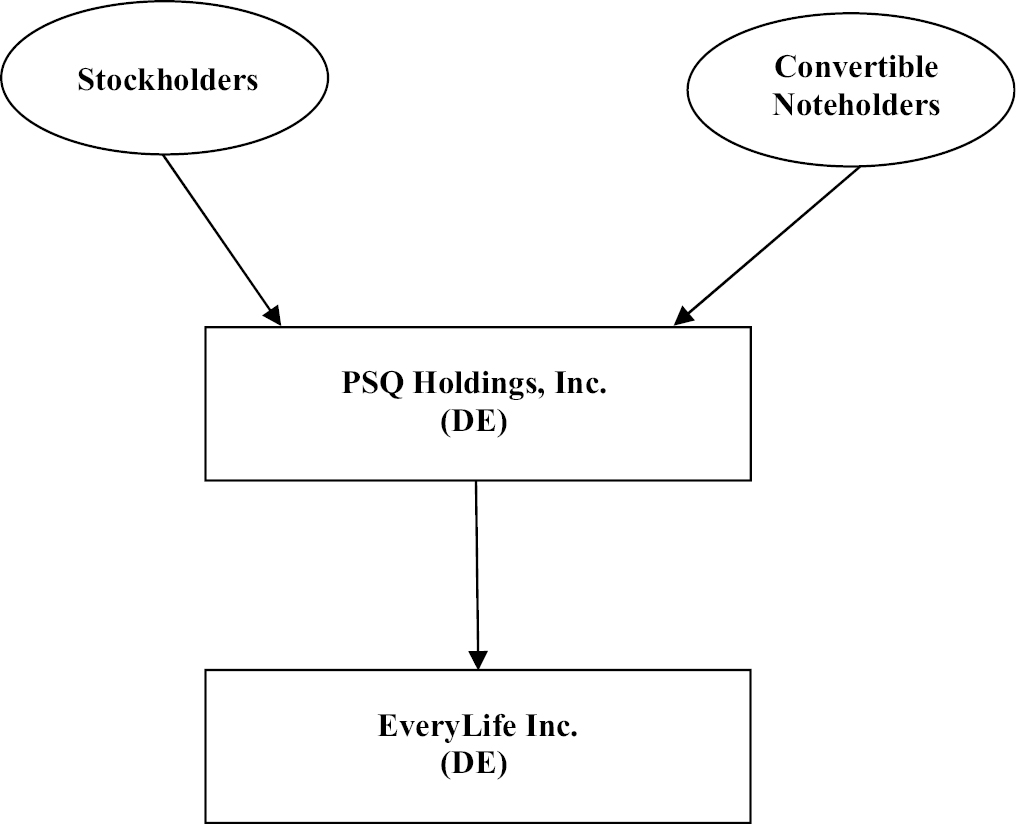

It is proposed that, at the closing of the Business Combination (the “Closing”), Colombier will change its name to “PSQ Holdings, Inc.” Colombier, following the Business Combination, is referred to herein as the “Company” or the “Combined Company.”

Pursuant to the terms of the Merger Agreement, upon satisfaction (or waiver) of the conditions to Closing set forth therein, at the effective time of the Merger (as defined below) (the “Effective Time”), Merger Sub will merge with and into PSQ (the “Merger”), with PSQ surviving the Merger as a wholly-owned subsidiary of Colombier. As a result of and upon the Effective Time, among other things, any PSQ Convertible Securities (as defined below) which remain outstanding and have not been exercised or do not convert automatically into shares of PSQ Common Stock (as defined below) prior to the Effective Time will be cancelled without consideration; each share of PSQ Common Stock, par value $0.001 per share (“PSQ Common Stock”), other than shares held by Michael Seifert, PSQ’s Founder and Chief Executive Officer (the “PSQ Founder”), will be cancelled and converted into the right to receive a number of shares of Class A Common Stock, par value $0.0001 per share, of the Combined Company (“Class A Common Stock”) equal to the Conversion Ratio (as defined in the Merger Agreement); and each share of PSQ Common Stock held by the PSQ Founder will be cancelled and converted into the right to receive a number of shares of Class C Common Stock, par value $0.0001 per share, of the Combined Company (“Class C Common Stock” and, together with the Class A Common Stock, the “Combined Company Common Stock”), equal to the Conversion Ratio.

The total consideration to be received by security holders of PSQ at the Closing in connection with the Merger (the “Merger Consideration”) will be a number of newly issued shares of Combined Company Common Stock with an aggregate value equal to $200,000,000, subject to adjustments for PSQ’s closing debt (net of cash), and based on a deemed value of $10.00 per share of Combined Company Common Stock. In addition to the right to receive Class A Common Stock or Class C Common Stock, as applicable, in the Merger, holders of PSQ Common Stock and certain other employees and service providers of PSQ (collectively, the “Participating Equityholders”) will be entitled to receive up to 3,000,000 shares of Class A Common Stock (the “Earnout Shares”) in the event certain metrics are satisfied during the five-year period commencing on the date of the Closing and ending on the fifth anniversary thereof (the “Earnout Period”), or, if earlier, upon the occurrence of a change of control transaction during the Earnout Period with an implied per share price that exceeds the relevant trading price-based metrics.

The proposed certificate of incorporation for the Combined Company intended to be in effect from and after the Closing (the “Proposed Charter”) provides that (i) the Combined Company’s Class A Common Stock and Class C Common Stock will vote together as a single class on substantially all matters to be voted on by the Combined Company’s

stockholders, (ii) on all such matters, each share of the Combined Company’s Class A Common Stock will entitle its holder to one vote per share and (iii) on all such matters, each share of the Combined Company’s Class C Common Stock (all of which will be held by the PSQ Founder immediately following the Closing) will entitle its holder to a number of votes per share (rounded up to the nearest whole number) equal to (a) the aggregate number of outstanding shares of Class A Common Stock entitled to vote on such matter plus 100, divided by (b) the aggregate number of outstanding shares of Class C Common Stock.

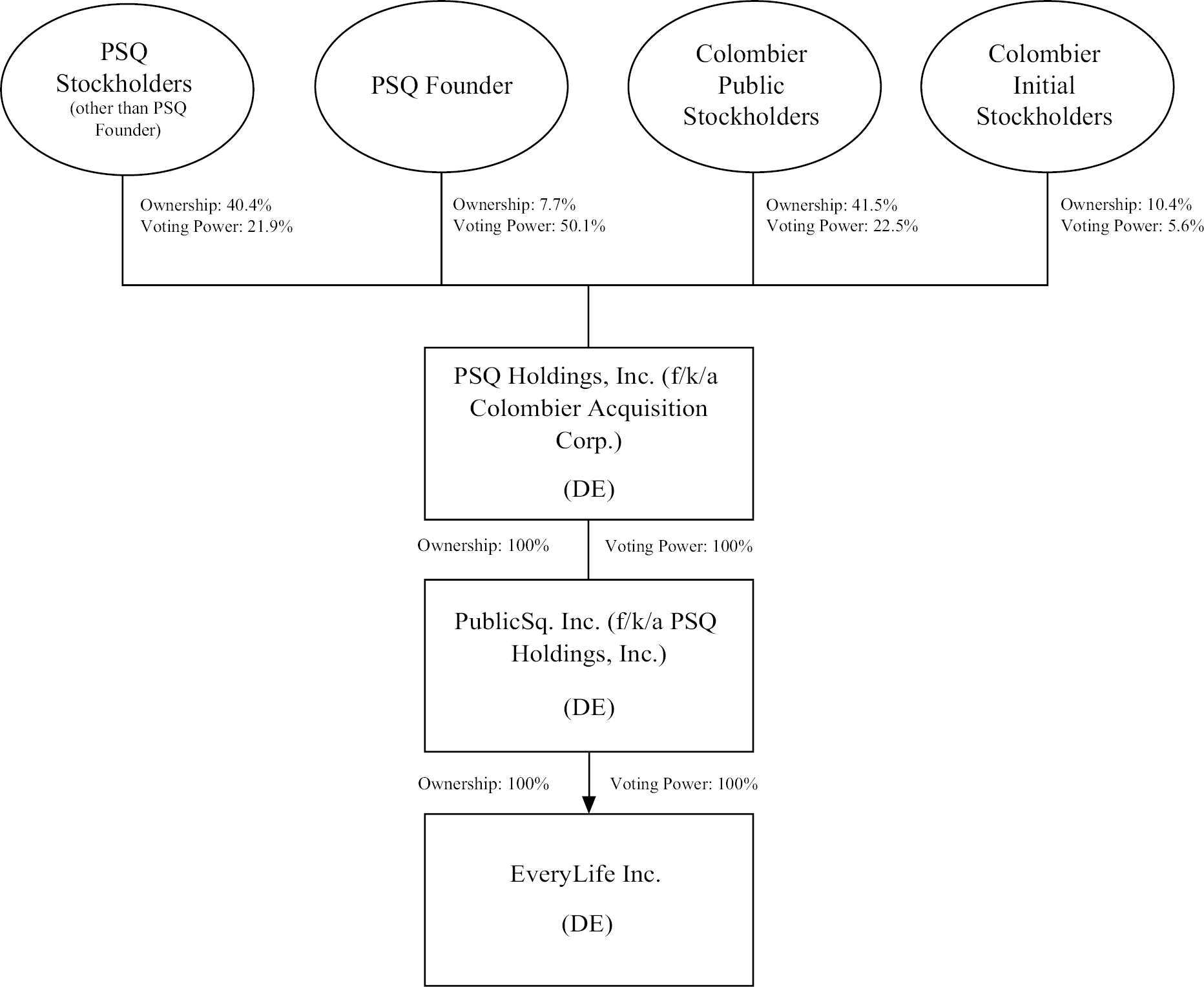

It is anticipated that upon completion of the Business Combination, the Colombier public stockholders would retain an ownership interest of approximately 41.5% in the Combined Company, the Sponsor will retain an ownership interest of approximately 10.4% of the Combined Company, and the holders of PSQ Common Stock immediately prior to the Effective Time (the “PSQ Stockholders”) will have ownership of approximately 48.1% of the Combined Company. It is anticipated that upon completion of the Business Combination, as a result of the Combined Company’s dual class common stock structure, Colombier public stockholders would retain voting power of approximately 22.5% of the Combined Company, the Sponsor would retain voting power of approximately 5.6% of the Combined Company, the PSQ Stockholders holding shares of the Combined Company’s Class A Common Stock would have voting power of approximately 21.9% of the Combined Company and Mr. Seifert, as the holder of all of the outstanding shares of the Combined Company’s Class C Common Stock, would have voting power of approximately 50.1% of the Combined Company (such that all of the former PSQ Stockholders together would have voting power of approximately 71.9% of the Combined Company). The ownership and voting percentages with respect to the Combined Company do not take into account the redemption of any shares by Colombier public stockholders. If the actual facts are different from these assumptions (which they are likely to be), the percentage of ownership and voting power retained by the Colombier stockholders will be different. See “Share Calculations and Ownership Percentages” and “Unaudited Pro Forma Condensed Combined Financial Information.”

Following consummation of the Business Combination, as a result of his ownership of all of the outstanding shares of Class C Common Stock, the PSQ Founder is expected to control all matters to be voted upon by the Combined Company’s stockholders (except for certain matters (such as amendments to the Proposed Charter) which require a supermajority vote or the approval of both the Class A Common Stock and Class C Common Stock voting as separate classes, with respect to which the holders of the Class C Common Stock will have sufficient voting power to prevent, but not on their own approve). As a result, the Combined Company will be a “controlled company” as defined in the corporate governance rules of the NYSE.

Colombier’s Units, Colombier Class A Common Stock and Colombier’s public warrants are traded on the New York Stock Exchange (“NYSE”) under the symbols “CLBR.U,” “CLBR” and “CLBR.WS,” respectively. On [•], 2023, the record date for the Colombier Special Meeting (the “Record Date”), the closing sale prices of Colombier’s Units, shares of Colombier Class A Common Stock and Colombier’s public warrants were $[•], $[•] and $[•], respectively. Upon the Closing, Colombier’s Units will be separated into their component securities and cease to exist as separate securities. Colombier intends to apply for the listing of the Class A Common Stock and warrants of the Combined Company following completion of the Business Combination on the NYSE or any applicable national securities exchange.

Only holders of record of shares of Colombier Class A Common Stock and Colombier Class B Common Stock at the close of business on [•], 2023 are entitled to notice of the Colombier Special Meeting and the right to vote and have their votes counted at the Colombier Special Meeting and any adjournments or postponements of the Colombier Special Meeting.

The accompanying proxy statement/prospectus provides Colombier stockholders with detailed information about the Business Combination and other matters to be considered at the Colombier Special Meeting. Colombier urges its stockholders to carefully read this entire document and the documents incorporated herein by reference. Colombier stockholders should also carefully consider the risk factors described in “Risk Factors” beginning on page 56 of the accompanying proxy statement/prospectus.

The accompanying proxy statement/prospectus may refer to important business and financial information about Colombier reflected in documents Colombier has filed with the Securities and Exchange Commission that are not included in or delivered with this proxy statement/prospectus. You may access these and other filings of Colombier with the Securities and Exchange Commission by visiting its website at www.sec.gov or by requesting them from in writing or by telephone at the following address:

Morrow Sodali LLC

333 Ludlow Street, 5th Floor, South Tower

Stamford, CT 06902

Tel: (800) 662-5200 (toll-free) or

(203) 658-9400 (banks and brokers can call collect)

Email: CLBR.info@investor.morrowsodali.com

You will not be charged for any of these documents that you request. Stockholders requesting documents should do so by [•], 2023 in order to receive them before the Colombier Special Meeting.

After careful consideration, the Colombier Board has unanimously approved the Merger Agreement and the Business Combination and determined that each of the proposals described in the accompanying proxy statement/prospectus is in the best interests of Colombier and recommends that you vote “FOR” each of these Proposals.

The accompanying proxy statement/prospectus provides Colombier stockholders with detailed information about the Business Combination and other matters to be considered at the Colombier Special Meeting. Colombier urges you to read the accompanying proxy statement/prospectus, including the financial statements and annexes and other documents referred to therein, carefully and in their entirety. In particular, when you consider the recommendation regarding these Proposals by the Colombier Board, you should keep in mind that Colombier’s directors and officers have interests in the Business Combination that are different from or in addition to, or may conflict with, your interests as a Colombier stockholder. For instance, rather than liquidating Colombier, the Sponsor will benefit from the completion of the Business Combination and may be incentivized to complete the Business Combination, even if the transaction is unfavorable to stockholders of Colombier. In addition, you should carefully consider the matters discussed under “Risk Factors” beginning on page 56 of the accompanying proxy statement/prospectus. See also the section entitled “The Business Combination Proposal — Interests of Colombier’s Sponsor, Directors and Officers and Advisors in the Business Combination” for additional information.

Your vote is very important. To ensure your representation at the Colombier Special Meeting, please complete and return the enclosed proxy card or submit your proxy by following the instructions contained in the accompanying proxy statement/prospectus and on your proxy card. Please submit your proxy promptly whether or not you expect to participate in the meeting. Submitting a proxy now will NOT prevent you from being able to vote online during the virtual Colombier Special Meeting. If you hold your shares in “street name,” you should instruct your broker, bank or other nominee how to vote in accordance with the voting instruction form you receive from your broker, bank or other nominee.

|

Very truly yours, |

||

|

|

||

|

Omeed Malik |

||

|

Chief Executive Officer and Chairman of the Board |

If you return your proxy card signed and without an indication of how you wish to vote, your shares will be voted in favor of each of the proposals and for the election of each of the directors proposed by Colombier for election.

TO EXERCISE YOUR REDEMPTION RIGHTS, YOU MUST (1) IF YOU HOLD SHARES OF COLOMBIER CLASS A COMMON STOCK THROUGH UNITS, SEPARATE YOUR UNITS INTO THE UNDERLYING SHARES OF COLOMBIER CLASS A COMMON STOCK AND PUBLIC WARRANTS PRIOR TO EXERCISING YOUR REDEMPTION RIGHTS WITH RESPECT TO THE PUBLIC SHARES, (2) SUBMIT A WRITTEN REQUEST, INCLUDING THE LEGAL NAME, PHONE NUMBER AND ADDRESS OF THE BENEFICIAL OWNER OF THE SHARES FOR WHICH REDEMPTION IS REQUESTED, TO THE TRANSFER AGENT AT LEAST TWO BUSINESS DAYS PRIOR TO THE DATE OF THE COLOMBIER SPECIAL MEETING, THAT YOUR PUBLIC SHARES BE REDEEMED FOR CASH AND (3) DELIVER YOUR STOCK CERTIFICATES (IF ANY) AND OTHER REDEMPTION FORMS TO THE TRANSFER AGENT, PHYSICALLY OR ELECTRONICALLY USING THE DEPOSITORY TRUST COMPANY’S DWAC (DEPOSIT/WITHDRAWAL AT CUSTODIAN) SYSTEM, IN EACH CASE, IN ACCORDANCE WITH THE PROCEDURES AND DEADLINES DESCRIBED IN THE PROXY STATEMENT/PROSPECTUS. IF THE BUSINESS COMBINATION IS NOT CONSUMMATED, THEN THE PUBLIC SHARES WILL NOT BE REDEEMED FOR CASH. IF YOU HOLD THE SHARES IN STREET NAME, YOU WILL NEED TO INSTRUCT THE ACCOUNT EXECUTIVE AT YOUR BANK, BROKER OR OTHER NOMINEE TO WITHDRAW THE SHARES FROM YOUR ACCOUNT IN ORDER TO EXERCISE YOUR REDEMPTION RIGHTS. SEE “THE COLOMBIER SPECIAL MEETING — REDEMPTION RIGHTS” IN THE PROXY STATEMENT/PROSPECTUS FOR MORE SPECIFIC INSTRUCTIONS.

Neither the U.S. Securities and Exchange Commission nor any state securities commission has approved or disapproved of the Business Combination or the other transactions contemplated thereby, as described in the accompanying proxy statement/prospectus, or passed upon the adequacy or accuracy of the disclosure in the accompanying proxy statement/prospectus. Any representation to the contrary is a criminal offense.

The accompanying proxy statement/prospectus is dated [•], 2023, and is first being mailed to stockholders of Colombier on or about [•], 2023.

Colombier Acquisition Corp.

214 Brazilian Avenue, Suite 200-J

Palm Beach, FL 33480

NOTICE OF SPECIAL MEETING OF STOCKHOLDERS

To Be Held On [•], 2023

[•] a.m. Eastern Time

[•], 2023

TO THE STOCKHOLDERS OF COLOMBIER ACQUISITION CORP.:

NOTICE IS HEREBY GIVEN that a special meeting of stockholders (the “Colombier Special Meeting”) of Colombier Acquisition Corp., a Delaware corporation (“Colombier”), will be held virtually at [•] a.m. Eastern Time on [•], 2023. The Colombier Board of Directors (the “Colombier Board”) has determined to convene and conduct the Colombier Special Meeting in a virtual meeting format at www.cstproxy.com/Colombier/[•]. Stockholders will NOT be able to attend the Colombier Special Meeting in-person. The accompanying proxy statement/prospectus includes instructions on how to access the virtual Colombier Special Meeting and how to listen and vote from home or any remote location with internet connectivity. You or your proxy holder will be able to attend and vote at the Colombier Special Meeting by visiting www.cstproxy.com/[•] and using a control number assigned by Continental Stock Transfer & Trust Company. The Colombier Special Meeting will be held for the purpose of considering and voting on the proposals (the “Proposals”) described below and in the accompanying proxy statement/prospectus. To register and receive access to the virtual meeting, registered stockholders and beneficial stockholders (those holding shares through a stock brokerage account or by a bank or other holder of record) of Colombier will need to follow the instructions applicable to them provided in the accompanying proxy statement/prospectus. At the Colombier Special Meeting, Colombier stockholders will be asked to consider and vote upon the following Proposals:

(i) The NTA Proposal (Proposal 1) — To consider and vote on the approval and adoption of the amendments to the current Certificate of Incorporation of Colombier (as amended from time to time, the “Current Charter”), which amendments (the “NTA Amendments”) shall be effective, if adopted and implemented by Colombier, prior to the consummation of the proposed Business Combination, to remove from the Current Charter requirements limiting Colombier’s ability to redeem shares of Colombier Class A Common Stock and consummate an initial business combination if the amount of such redemptions would cause Colombier to have less than $5,000,001 in net tangible assets (“NTA”). The NTA Proposal is conditioned upon the approval of the Business Combination Proposal. Therefore, if the Business Combination Proposal is not approved, then the NTA Proposal will have no effect, even if approved by Colombier stockholders. The NTA Proposal is described in more detail in the accompanying proxy statement/prospectus under the heading “The NTA Proposal (Proposal 1).”

(ii) The Business Combination Proposal (Proposal 2) — To consider and vote on a proposal to approve and adopt the Agreement and Plan of Merger, dated as of February 27, 2023 (as it may be amended or supplemented from time to time, the “Merger Agreement”), by and among Colombier, Colombier-Liberty Acquisition, Inc., a Delaware corporation and wholly-owned subsidiary of Colombier (“Merger Sub”), Colombier Sponsor, LLC, a Delaware limited liability company (the “Sponsor”), in its capacity as Purchaser Representative (the “Purchaser Representative”) for the purposes set forth in the Merger Agreement, and PSQ Holdings, Inc., a Delaware corporation (“PSQ”), and approve the transactions contemplated thereby, including the merger of Merger Sub with and into PSQ, with PSQ continuing as the surviving corporation and as a wholly-owned subsidiary of Colombier, and the issuance of Colombier securities as Merger Consideration thereunder, as described in more detail in the accompanying proxy statement/prospectus (the “Merger” and, together with the other transactions contemplated by the Merger Agreement, the “Business Combination”).

The Business Combination Proposal is described in more detail in the accompanying proxy statement/prospectus under the heading “The Business Combination Proposal (Proposal 2).” A copy of the Merger Agreement is attached to the accompanying proxy statement/prospectus as Annex A.

(iii) The Charter Proposal (Proposal 3) — To consider and vote upon a proposal to approve and adopt, in connection with the Business Combination, the proposed new amended and restated certificate of

incorporation of Colombier (the “Proposed Charter”) in the form attached to the accompanying proxy statement/prospectus as Annex B. The Charter Proposal is conditioned on the approval of the Business Combination Proposal. Therefore, if the Business Combination Proposal is not approved, then the Charter Proposal will have no effect, even if approved by Colombier stockholders. The Charter Proposal is described in more detail in the accompanying proxy statement/prospectus under the heading “The Charter Proposal (Proposal 3).”

(iv) Advisory Charter Proposals (Proposals 4 – 7) — To consider and vote, on an advisory and non-binding basis, on four separate Proposals to approve certain governance provisions in the Proposed Charter. These separate votes are not otherwise required by Delaware law, separate and apart from the Charter Proposal, but are required by SEC guidance requiring that stockholders have the opportunity to present their views on important corporate governance provisions. The Business Combination is not conditioned on the separate approval of the Advisory Charter Proposals (separate and apart from approval of the Charter Proposal). The Advisory Charter Proposals are described in more detail in the accompanying proxy statement/prospectus under the heading “The Advisory Charter Proposals (Proposals 4 – 7).”

(v) The Incentive Plan Proposal (Proposal 8) — To consider and vote upon a proposal to approve the 2023 Stock Incentive Plan (the “Incentive Plan”), the form of which is attached to the accompanying proxy statement/prospectus. The Colombier Board intends to adopt the Incentive Plan, subject to the approval of the Colombier stockholders. If adopted and approved, the Incentive Plan will be effective upon the Closing. The Incentive Plan Proposal is described in more detail in the accompanying proxy statement/prospectus under the heading “The Incentive Plan Proposal (Proposal 8).”

(vi) The ESPP Proposal (Proposal 9) — To consider and vote upon a proposal to approve the 2023 Employee Stock Purchase Plan (the “ESPP”), the form of which is attached to the accompanying proxy statement/prospectus. The Colombier Board intends to adopt the ESPP, subject to the approval of the Colombier stockholders. If adopted and approved, the ESPP will be effective upon the Closing. The ESPP Proposal is described in more detail in the accompanying proxy statement/prospectus under the heading “The ESPP Proposal (Proposal 9).”

(vii) The NYSE Proposal (Proposal 10) — To consider and vote upon, for purposes of complying with the applicable listing rules of the New York Stock Exchange (the “NYSE”), the issuance of the shares of Class A Common Stock and Class C Common Stock to be issued in connection with the Business Combination. The NYSE Proposal is described in more detail in the accompanying proxy statement/prospectus under the heading “NYSE Proposal (Proposal 10).”

(x) The Adjournment Proposal (Proposal 11) — To consider and vote upon a proposal to adjourn the Colombier Special Meeting to a later date or dates, if necessary, at the determination of the Colombier Board or the chairman of the Colombier Special Meeting. We refer to this proposal as the “Adjournment Proposal.”

Only holders of record of the Class A Common Stock, par value $0.0001 per share, of Colombier (the “Colombier Class A Common Stock”), and the Class B Common Stock, par value $0.0001 per share, of Colombier (the “Colombier Class B Common Stock” and together with the Colombier Class A Common Stock, the “Colombier Common Stock”) at the close of business on [•], 2023 (“Record Date”) are entitled to notice of the Colombier Special Meeting and to vote at the Colombier Special Meeting and any adjournments or postponements of the Colombier Special Meeting. A complete list of Colombier stockholders of record entitled to vote at the Colombier Special Meeting will be available for ten days before the Colombier Special Meeting at the principal executive offices of Colombier for inspection by stockholders during ordinary business hours for any purpose germane to the Colombier Special Meeting.

Pursuant to the Current Charter, in connection with the Business Combination, Colombier public stockholders may elect to have Colombier redeem, effective upon the closing of the Business Combination, shares of Colombier Class A Common Stock then held by them for cash equal to a pro rata portion of the aggregate amount on deposit in the Trust Account as of two (2) business days prior to the consummation of the Business Combination, including interest earned on the funds held in the Trust Account and not previously released to Colombier in connection with Permitted Withdrawals, divided by the number of then outstanding public shares, subject to the limitations described herein. As of May 18, 2023, based on funds in the Trust Account of approximately $174.87 million as of such date, the pro rata portion of the funds available in the Trust Account for the redemption of public shares of Colombier Class A Common

Stock was approximately $10.14 per share. Colombier public stockholders are not required to attend or vote at the Colombier Special Meeting in order to elect to have Colombier redeem their shares of Colombier Class A Common Stock for cash. This means that public stockholders who hold shares of Colombier Class A Common Stock on or before [•], 2023 (two (2) business days before the Colombier Special Meeting) will be eligible to elect to have their shares of Colombier Class A Common Stock redeemed for cash in connection with the Colombier Special Meeting, whether or not they are holders as of the Record Date, and whether or not such shares are voted at the Colombier Special Meeting. A public stockholder, together with any of such stockholder’s affiliates or any other person with whom such public stockholder is acting in concert or as a “group” (as defined under Section 13 of the Securities Exchange Act of 1934, as amended (the “Exchange Act”)), will be restricted from electing to have shares redeemed without Colombier’s prior consent if, in the aggregate such stockholder’s shares or, if part of such a group, the group’s shares, for which redemption is sought exceeds 15% or more of the shares of Colombier Common Stock included in the units of Colombier sold in the Colombier initial public offering (the “IPO”) (including overallotment securities sold to Colombier’s underwriters in connection with the IPO). Holders of Colombier’s outstanding public warrants and Units do not have redemption rights with respect to such securities in connection with the Business Combination. Holders of outstanding Colombier Units must separate the underlying shares of Colombier Class A Common Stock and public warrants prior to exercising redemption rights with respect to the public Colombier Class A Common Stock.

The Sponsor and Colombier’s officers and directors have agreed to waive their redemption rights with respect to any shares of Colombier Class A Common Stock they may hold in connection with the consummation of the Business Combination, and such shares will be excluded from the pro rata calculation used to determine the per share redemption price. Currently, the Sponsor and Colombier’s officers and directors beneficially own 20% of the issued and outstanding shares of Colombier Class A Common Stock, giving effect to the conversion from Colombier Class B Common Stock immediately prior to the effective time of the Merger (the “Effective Time”) at a one-to-one conversion ratio. The Sponsor has also agreed to waive its anti-dilution rights that would otherwise allow the Sponsor to maintain ownership of 20% of the Combined Company. The Sponsor and Colombier’s officers and directors have agreed to vote any shares of Colombier Common Stock owned by them on the Record Date in favor of the Business Combination and the other Proposals.

Your vote is very important, regardless of the number of shares of Colombier Class A Common Stock that you own. The approval of the NTA Proposal requires the affirmative vote of holders of sixty-five percent (65%) of the issued and outstanding shares of Colombier Common Stock as of the Record Date, voting as a single class. The approval of the Business Combination Proposal requires the affirmative vote of holders of a majority of the shares of the Colombier Common Stock that are voted at the Colombier Special Meeting, voting together as a single class. The approval of the Charter Proposal requires the affirmative vote of holders of (i) at least a majority of the issued and outstanding shares of Colombier Common Stock as of the Record Date, voting as a single class, (ii) at least a majority of the issued and outstanding shares of Colombier Class A Common Stock as of the Record Date, voting as a separate class and (iii) at least a majority of the issued and outstanding shares of Colombier Class B Common Stock as of the Record Date, voting as a separate class. Assuming a quorum is present, approval of the Advisory Charter Proposals, the Incentive Plan Proposal, the ESPP Proposal, the NYSE Proposal and the Adjournment Proposal each requires a majority of the votes cast thereon by the holders of the shares of Colombier Common Stock represented in person online or by proxy and entitled to vote thereon at the Colombier Special Meeting, voting together as a single class.

If the Business Combination Proposal is not approved, the Charter Proposal, the Advisory Charter Proposals, the Incentive Plan Proposal, the ESPP Proposal and the NYSE Proposal will not be presented to the Colombier stockholders for a vote. The NTA Proposal is conditioned upon the approval of the Business Combination Proposal. Therefore, if the Business Combination Proposal is not approved, then the NTA Proposal will have no effect, even if approved by Colombier stockholders. The approval of the Business Combination Proposal and the Charter Proposal, the Incentive Plan Proposal, the ESPP Proposal and the NYSE Proposal are preconditions to the consummation of the Business Combination.

The Colombier Board has adopted and approved the Merger Agreement and recommends that Colombier stockholders vote “FOR” all of the Proposals presented to Colombier stockholders at the Colombier Special Meeting. In arriving at its recommendations, the Colombier Board carefully considered a number of factors described in the accompanying proxy statement/prospectus. When you consider the recommendation of the Colombier Board, you should keep in mind that directors and officers of Colombier have interests in the Business Combination that may conflict with your interests as a stockholder. For instance, rather than liquidating Colombier, the Sponsor will benefit from the Business Combination and may be incentivized to complete the Business Combination, even if the transaction is unfavorable to stockholders. See the section entitled “The Business Combination Proposal — Interests of Colombier’s Sponsor, Directors and Officers and Advisors in the Business Combination” for a further discussion of these considerations.

All Colombier stockholders are cordially invited virtually to attend the Colombier Special Meeting and we are providing the accompanying proxy statement/prospectus and proxy card in connection with the solicitation of proxies to be voted at the Colombier Special Meeting (or any adjournment or postponement thereof). To ensure your representation at the Colombier Special Meeting, however, you are urged to complete, sign, date and return the enclosed proxy card as soon as possible. If your shares are held in an account at a brokerage firm, bank or other nominee, you must instruct your broker, bank or other nominee on how to vote your shares or, if you wish to virtually attend the Colombier Special Meeting and vote, obtain a proxy from your broker, bank or other nominee.

Your vote is important regardless of the number of shares you own. Whether you plan to attend the Colombier Special Meeting or not, please sign, date and return the enclosed proxy card as soon as possible in the envelope provided. If your shares are held in “street name” or are in a margin or similar account, you should contact your broker to ensure that votes related to the shares you beneficially own are properly counted.

Your attention is directed to the proxy statement/prospectus accompanying this notice (including the annexes thereto) for a more complete description of the proposed Business Combination and related transactions and each of the proposals. We encourage you to read this proxy statement/prospectus carefully. If you have any questions or need assistance voting your shares, please contact Morrow Sodali LLC, our proxy solicitor, using the contact information provided in the enclosed proxy statement/prospectus.

|

By Order of the Board of Directors of Colombier |

||

|

|

||

|

Omeed Malik |

||

|

Chief Executive Officer and Chairman of the Board |

IF YOU RETURN YOUR PROXY CARD WITHOUT AN INDICATION OF HOW YOU WISH TO VOTE, YOUR SHARES WILL BE VOTED IN FAVOR OF EACH OF THE PROPOSALS.

TO EXERCISE YOUR REDEMPTION RIGHTS, YOU MUST (1) IF YOU HOLD SHARES OF COLOMBIER CLASS A COMMON STOCK THROUGH UNITS, ELECT TO SEPARATE YOUR UNITS INTO THE UNDERLYING SHARES OF COLOMBIER CLASS A COMMON STOCK AND PUBLIC WARRANTS PRIOR TO EXERCISING YOUR REDEMPTION RIGHTS WITH RESPECT TO THE PUBLIC SHARES, (2) SUBMIT A WRITTEN REQUEST, INCLUDING THE LEGAL NAME, PHONE NUMBER AND ADDRESS OF THE BENEFICIAL OWNER OF THE SHARES FOR WHICH REDEMPTION IS REQUESTED, TO THE TRANSFER AGENT AT LEAST TWO BUSINESS DAYS PRIOR TO THE VOTE AT THE COLOMBIER SPECIAL MEETING, THAT YOUR PUBLIC SHARES BE REDEEMED FOR CASH AND (3) DELIVER YOUR STOCK CERTIFICATES (IF ANY) AND OTHER REDEMPTION FORMS TO THE TRANSFER AGENT, PHYSICALLY OR ELECTRONICALLY USING THE DEPOSITORY TRUST COMPANY’S DWAC (DEPOSIT/WITHDRAWAL AT CUSTODIAN) SYSTEM, IN EACH CASE, IN ACCORDANCE WITH THE PROCEDURES AND DEADLINES DESCRIBED IN THE PROXY STATEMENT/PROSPECTUS. IF THE BUSINESS COMBINATION IS NOT CONSUMMATED, THEN THE PUBLIC SHARES WILL NOT BE REDEEMED FOR CASH. IF YOU HOLD THE SHARES IN STREET NAME, YOU WILL NEED TO INSTRUCT THE ACCOUNT EXECUTIVE AT YOUR BANK, BROKER OR OTHER NOMINEE TO WITHDRAW THE SHARES FROM YOUR ACCOUNT IN ORDER TO EXERCISE YOUR REDEMPTION RIGHTS. SEE “THE COLOMBIER SPECIAL MEETING — REDEMPTION RIGHTS’’ IN THIS PROXY STATEMENT/PROSPECTUS FOR MORE SPECIFIC INSTRUCTIONS.

ABOUT THIS DOCUMENT

This document, which forms part of a registration statement on Form S-4 filed with the Securities and Exchange Commission (the “SEC”) by Colombier, constitutes a prospectus of Colombier under the Securities Act of 1933, as amended (the “Securities Act”), with respect to the shares of Colombier Common Stock to be issued to PSQ securityholders under the Merger Agreement. This document also constitutes a notice of a meeting and a proxy statement of Colombier under Section 14(a) of the Exchange Act with respect to the Colombier Special Meeting at which Colombier stockholders will be asked to consider and vote on a Proposal to approve and adopt the Business Combination by the approval and adoption of the Merger Agreement, among other matters.

This proxy statement/prospectus is dated as of the date set forth on the cover hereof. You should not assume that the information contained in this proxy statement/prospectus is accurate as of any date other than that date on the cover hereof, or the date referenced herein, as applicable. You should not assume that the information incorporated by reference into this proxy statement/prospectus is accurate as of any date other than the date of such incorporated document. Neither the mailing of this proxy statement/prospectus to Colombier stockholders nor the issuance by Colombier of its securities in connection with the Business Combination will create any implication to the contrary.

Information contained in this proxy statement/prospectus regarding Colombier and its business, operations, management and other matters has been provided by Colombier and its representatives and information contained in this proxy statement/prospectus regarding PSQ and its business, operations, management and other matters has been provided by PSQ and its representatives.

This proxy statement/prospectus does not constitute an offer to sell or a solicitation of an offer to buy any securities, or the solicitation of a proxy or consent, in any jurisdiction to or from any person to whom it is unlawful to make any such offer or solicitation in such jurisdiction.

If you would like additional copies of this proxy statement/prospectus or if you have questions about the Business Combination or the Proposals to be presented at the Colombier Special Meeting, please contact Colombier’s proxy solicitor listed below. You will not be charged for any of the documents that you request.

Morrow Sodali LLC

333 Ludlow Street, 5th Floor, South Tower

Stamford, CT 06902

Tel: (800) 662-5200 (toll-free) or

(203) 658-9400 (banks and brokers can call collect)

Email: CLBR.info@investor.morrowsodali.com

In order for you to receive timely delivery of the documents in advance of the Colombier Special Meeting to be held on [•], 2023, you must request the information by [•], 2023.

For a more detailed description of the information incorporated by reference in this proxy statement/prospectus and how you may obtain it, see the section captioned “Where You Can Find More Information” beginning on page 283 of this proxy statement/prospectus.

TABLE OF CONTENTS

|

Page |

||

|

1 |

||

|

1 |

||

|

2 |

||

|

9 |

||

|

12 |

||

|

33 |

||

|

47 |

||

|

50 |

||

|

51 |

||

|

SUMMARY UNAUDITED PRO FORMA CONDENSED COMBINED FINANCIAL INFORMATION |

53 |

|

|

55 |

||

|

56 |

||

|

UNAUDITED PRO FORMA CONDENSED COMBINED FINANCIAL INFORMATION |

112 |

|

|

NOTES TO UNAUDITED PRO FORMA CONDENSED COMBINED FINANCIAL STATEMENTS FOR DECEMBER 31, 2022 |

122 |

|

|

COMPARATIVE HISTORICAL AND UNAUDITED PRO FORMA PER SHARE FINANCIAL INFORMATION |

125 |

|

|

126 |

||

|

127 |

||

|

137 |

||

|

139 |

||

|

170 |

||

|

175 |

||

|

177 |

||

|

187 |

||

|

192 |

||

|

194 |

||

|

195 |

||

|

201 |

||

|

203 |

||

|

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS OF COLOMBIER |

210 |

|

|

216 |

||

|

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS OF psq |

228 |

|

|

244 |

||

|

253 |

||

|

254 |

||

|

262 |

||

|

265 |

||

|

272 |

||

|

276 |

||

|

278 |

||

|

281 |

||

|

281 |

||

|

281 |

i

|

Page |

||

|

281 |

||

|

281 |

||

|

282 |

||

|

282 |

||

|

282 |

||

|

283 |

||

|

F-1 |

||

|

A-1 |

||

|

B-1 |

||

|

C-1 |

||

|

D-1 |

||

|

E-1 |

ii

TRADEMARKS

This proxy statement/prospectus includes trademarks of PSQ such as PublicSq., EveryLife and others, which are protected under applicable intellectual property laws and are the property of PSQ or its subsidiaries. This proxy statement/prospectus also includes other trademarks, trade names and service marks that are the property of their respective owners. Solely for convenience, in some cases, the trademarks, trade names and service marks referred to in this proxy statement/prospectus are listed without the applicable ®, ™ and SM symbols, but they will assert, to the fullest extent under applicable law, their rights to these trademarks, trade names and service marks.

MARKET AND INDUSTRY DATA

This proxy statement/prospectus includes industry position, forecasts, market size and growth and other data that Colombier and PSQ obtained or derived from internal company reports, independent third-party reports and publications, surveys and studies by third parties and other industry data. Some data are also based on good faith estimates, which are derived from internal company research or analyses or review of internal company reports as well as the independent sources referred to above. Although both Colombier and PSQ believe that the information on which the companies have based these estimates of industry position and industry data are generally reliable, the accuracy and completeness of this information is not guaranteed and they have not independently verified any of the data from third-party sources nor have they ascertained the underlying economic assumptions relied upon therein. Colombier’s and PSQ’s internal company reports have not been verified by any independent source. Statements as to industry position are based on market data currently available. While Colombier and PSQ are not aware of any misstatements regarding the industry data presented herein, these estimates involve risks and uncertainties and are subject to change based on various factors, including those discussed under the heading “Risk Factors” in this proxy statement/prospectus.

1

FREQUENTLY USED TERMS

Unless otherwise stated or unless the context otherwise requires, the terms “we,” “us,” “our,” and “Colombier” refer to Colombier Acquisition Corp., and if the context requires, to the Combined Company following consummation of the Business Combination, which will be renamed “PSQ Holdings, Inc.”

In this document:

“Accounting Principles” means in accordance with GAAP as in effect at the date of the financial statement to which it refers or if there is no such financial statement, then as of the Closing Date, using and applying the same accounting principles, practices, procedures, policies and methods (with consistent classifications, judgments, elections, inclusions, exclusions and valuation and estimation methodologies) used and applied by the Target Companies in the preparation of the financial statements of the Target Companies represented to in the Merger Agreement.

“Administrative Support Agreement” means the agreement, dated June 8, 2021, between Colombier and Farvahar Capital pursuant to which Colombier agreed to pay Farvahar Capital a total of $10,000 per month for office space, administrative and support services.

“Aggregate Legal Reimbursement Cap” means that the total aggregate fees and expenses reimbursable, if any, by Colombier to B. Riley, on the one hand, or CF&CO, on the other hand, upon consummation of the Business Combination in respect of outside counsel legal fees pursuant to the B. Riley Engagement Letter and the CF&CO Engagement Letter shall not exceed $150,000.

“Ancillary Agreements” means each agreement, instrument or document attached to the Merger Agreement or executed or delivered by any party to the Merger Agreement in connection with or pursuant to the Merger Agreement.

“Business Combination” means the proposed business combination of Colombier and PSQ pursuant to the terms of the Merger Agreement and the other transactions contemplated by the Merger Agreement.

“B. Riley” means B. Riley Securities, Inc., in its capacity as non-exclusive financial advisor to Colombier in connection with the Business Combination.

“B. Riley Engagement Letter” means the engagement letter, dated as of January 19, 2023, pursuant to which Colombier engaged B. Riley to act as its non-exclusive financial advisor in connection with the Business Combination.

“B. Riley Reimbursable Expenses” means out-of-pocket fees and expenses reimbursable (subject to pre-approval by Colombier in the case of certain expenses, excluding outside counsel legal fees) by Colombier to B. Riley upon consummation, if any, of the Business Combination, not to exceed $150,000, in the aggregate, subject to the Aggregate Legal Reimbursement Cap and excluding reasonable and customary costs for background check expenses incurred by B. Riley on behalf of Colombier at Colombier’s request, which are reimbursable to B. Riley without limitation regardless of whether the proposed Business Combination is consummated.

“CF&CO” means Cantor Fitzgerald & Co., in its capacity as capital markets advisor to Colombier in connection with the Business Combination.

“CF&CO Engagement Letter” means the engagement letter, dated as of March 27, 2023, between Colombier and CF&CO pursuant to which Colombier engaged CF&CO to act as capital markets advisor to Colombier in connection with the Business Combination.

“CF&CO Reimbursable Expenses” means out of pocket fees and expenses reimbursable (subject to prior written consent by Colombier in the case of certain expenses, excluding outside counsel legal fees) by Colombier to CF&CO upon consummation, if any, of the Business Combination, not to exceed $150,000, in the aggregate, subject to the Aggregate Legal Reimbursement Cap.

“Class A Common Stock” means the shares of Class A common stock, par value $0.0001 per share, of the Combined Company.

“Class C Common Stock” means the shares of Class C common stock, par value $0.0001 per share, of the Combined Company.

“Closing” means the closing of the Business Combination.

2

“Closing Date” means the date of the Closing of the Business Combination.

“Closing Net Indebtedness” means, as of the Reference Time, (i) the aggregate amount of all Indebtedness (as defined in the Merger Agreement) of the Target Companies, minus (ii) the Closing Company Cash (as defined in the Merger Agreement), in each case of clauses (i) and (ii), on a consolidated basis and as determined in accordance with the Accounting Principles. For the avoidance of doubt, the Closing Net Indebtedness can be a negative number.

“Code” means the Internal Revenue Code of 1986, as amended.

“Colombier” means Colombier Acquisition Corp., a Delaware corporation, which will be renamed “PSQ Holdings, Inc.” following the Closing.

“Colombier Board” means the board of directors of Colombier prior to the Business Combination.

“Colombier Class A Common Stock” means the Class A Common Stock, par value $0.0001 per share, of Colombier, prior to the Business Combination.

“Colombier Class B Common Stock” means the Class B Common Stock, par value $0.0001 per share, of Colombier, prior to the Business Combination.

“Colombier Common Stock” means the Colombier Class A Common Stock and Colombier Class B Common Stock.

“Colombier Preferred Stock” means the preferred stock, par value $0.0001 per share, of Colombier, prior to the Business Combination.

“Colombier Securities” means the Units, the Colombier Common Stock, the Colombier Preferred Stock and the Warrants, collectively.

“Colombier Special Meeting” means the special meeting of the stockholders of Colombier, to be held virtually at [•] a.m., Eastern Time on [•], 2023.

“Colombier Sponsor Shares” means Colombier Class B Common Stock initially purchased by the Sponsor in the Private Placement prior to the IPO, and the shares of Colombier Class A Common Stock to be issued upon the conversion thereof in accordance with the terms of the Current Charter.

“Combined Company” refers to Colombier (which will be renamed PSQ Holdings, Inc. after the Business Combination, and which will include PSQ and any other direct or indirect subsidiaries of PSQ, to the extent applicable) from and after the Closing.

“Combined Company Board” refers to the board of directors of the Combined Company.

“Combined Company Common Stock” refers to the Class A Common Stock and the Class C Common Stock of the Combined Company subsequent to the Business Combination.

“Company Registration Rights Agreement” means the registration rights agreement to be entered into by Colombier, the Sponsor, PSQ and certain PSQ Stockholders party thereto, effective as of the Closing.

“Conversion Ratio” means the Per Share Price divided by $10.00, as such ratio will be determined as of the Closing Date.

“COVID-19 pandemic” means the SARS-CoV-2 pandemic.

“Current Charter” means Colombier’s certificate of incorporation filed with the Secretary of State of the State of Delaware on February 12, 2021, as amended on June 9, 2021.

“Deemed Equity Holder” means each of certain employees and service providers of PSQ, who will be entitled to receive fully vested shares of Class A Common Stock or another form of Earnout Equity Award under the Incentive Plan, provided they are then still providing services to the Combined Company, in the event that the Earnout Shares are earned in accordance with the terms of the Merger Agreement.

“DGCL” means the General Corporation Law of the State of Delaware, as amended.

3

“DTC” means The Depository Trust Company.

“DWAC” means The Depository Trust Company’s Deposit Withdrawal At Custodian.

“Earnout Equity Awards” means any equity awards issued to Deemed Equity Holders from the Earnout Subpool (as defined under the heading “The Incentive Plan Proposal (Proposal 8)” below, under the subheading “Description of the Incentive Plan”) to satisfy the Combined Company’s obligation to issue Earnout Shares to a Deemed Equity Holder.

“Earnout Shares” means up to 3,000,000 shares of Class A Common Stock that may be issued to Participating Equityholders upon achievement of certain trading price based targets for the Combined Company Common Stock following Closing.

“Effective Time” means the effective time of the Merger in accordance with the Merger Agreement.

“Equity Value” means (a) $200,000,000, minus (b) if the Closing Net Indebtedness is a positive number, the amount of Closing Net Indebtedness, plus (c) if the Closing Net Indebtedness is a negative number, the absolute value of the amount of the Closing Net Indebtedness.

“ESPP” means the 2023 Employee Stock Purchase Plan of the Combined Company, in the form included as Annex E to this proxy statement/prospectus.

“Exchange Act” means the Securities Exchange Act of 1934, as amended.

“Exchange Agent” means Continental Stock Transfer & Trust Company, or another agent appointed by Colombier and reasonably acceptable to PSQ for the purposes, and to perform the actions and transactions, described in the Merger Agreement in connection with the Closing.

“Farvahar Capital” or “Farvahar Partners” means Farvahar Capital LLC, an affiliate of the Sponsor.

“FINRA” means Financial Industry Regulatory Authority.

“GAAP” means generally accepted accounting principles in the United States.

“Fully-Diluted PSQ Shares” means the total number of issued and outstanding shares of PSQ Common Stock as of immediately prior to the Effective Time, after treating all outstanding PSQ Convertible Securities (to the extent not canceled as part of the Merger) as having been exercised or converted, as the case may be.

“HSR Act” means the Hart-Scott-Rodino Antitrust Improvements Act of 1976, as amended.

“Incentive Plan” means the 2023 Stock Incentive Plan of the Combined Company, in the form included as Annex D to this proxy statement/prospectus.

“Insider Letter” means the letter agreement, dated June 8, 2021, by and among Colombier, its officers and directors, and the Sponsor.

“Insiders” means Colombier’s officers and directors (at the time of the IPO), the Sponsor and each transferee of Colombier Sponsor Shares.

“IPO” means the initial public offering of Colombier’s securities that it consummated on June 11, 2021.

“IPO Prospectus” means the final prospectus of Colombier, dated June 8, 2021 in connection with the IPO, as filed with the SEC pursuant to Rule 424(b) under the Securities Act on June 9, 2021 (File No. 333-254492).

“IPO Underwriter” means B. Riley Securities, Inc., which is also sometimes referred to herein as “B. Riley” in its capacity as financial advisor to Colombier in connection with the Business Combination.

“Lock-Up Agreements” means the lock-up agreements entered into concurrent with the execution of the Merger Agreement pursuant to which certain holders of shares of PSQ Common Stock agreed to certain transfer and other restrictions for a period of time after the Closing, as set forth in such agreements, as may be amended, modified or supplemented.

“Marcum” means Marcum LLP, Colombier’s independent registered public accounting firm.

4

“May Mutual Waiver Letter” means the waiver letter entered into by Colombier and PSQ, dated as of May 18, 2023, pursuant to which: (i) Colombier waived its right, pursuant to Section 8.1(e)(iii) of the Merger Agreement, to terminate the Merger Agreement in the event that Michael Seifert, the PSQ Founder and PSQ’s Chief Executive Officer, who is expected, after the Closing, to be Chief Executive Officer and Chairman of the Board of the Combined Company, has not executed and delivered an Employment Agreement and a Non-Competition Agreement (in each case to be effective as the Closing) in form and substance reasonably acceptable to Colombier on or on or prior to the date on which Colombier files the first amendment to this Registration Statement on Form S-4 with the SEC and (ii) PSQ waived its right, pursuant to Section 8.1(i) of the Merger Agreement, to terminate the Merger Agreement by written notice delivered to Colombier no later than May 22, 2023, in the event that PSQ has not received proceeds from a Permitted Financing in an amount equal to at least $15 million by May 15, 2023.

“Merger” means the merger of Merger Sub with and into PSQ, with PSQ continuing as the surviving corporation and as a wholly-owned subsidiary of Colombier, in accordance with the terms of the Merger Agreement.

“Merger Agreement” means the Agreement and Plan of Merger, dated as of February 27, 2023, as it may be amended or supplemented from time to time, by and among Colombier, Merger Sub, Sponsor, as purchaser representative, and PSQ.

“Merger Consideration” means the total number of shares of Class A Common Stock and Class C Common Stock into which the PSQ Common Stock will be converted into the right to receive at Closing pursuant to the Merger Agreement.

“Merger Sub” means Colombier-Liberty Acquisition Inc., a Delaware corporation and wholly-owned subsidiary of Colombier.

“Minimum Cash Condition” means one of the conditions to PSQ’s obligation to consummate the Merger, waivable by PSQ, that Colombier has cash and cash equivalents at least equal to (i) $33.0 million minus (ii) the lesser of (x) $15.0 million and (y) the amount of Colombier’s and PSQ’s aggregate unpaid transaction expenses immediately prior to the Closing, minus (iii) the amount of the proceeds actually received by PSQ in any Permitted Financing.

“NEO New Employment Agreements” means the executive employment agreements between Colombier and certain PSQ executives to be entered into and delivered to Colombier prior to the Closing, as may be amended, modified or supplemented.

“Non-Competition Agreements” means the non-competition and non-solicitation agreements to be entered into by certain executives of PSQ pursuant to the terms of the Merger Agreement.

“NYSE” means the New York Stock Exchange.

“Outside Date” means, for purposes of, and as used in, the Merger Agreement, the date of September 11, 2023, or an applicable later date (which shall not be later than December 31, 2023) if extended pursuant to the terms of the Merger Agreement.

“Participating Equityholder” means each PSQ Stockholder and each Deemed Equity Holder.

“Per Share Price” means the amount equal to the Equity Value divided by the Fully-Diluted PSQ Shares.

“Permitted Financing” means an equity or debt financing transaction or series of equity or debt financing transactions entered into by PSQ after the date of the Merger Agreement, by way of issuance, subscription or sale, which results in cash proceeds to PSQ prior to the Effective Time.

“Permitted Withdrawals” means, as applicable, withdrawals from the principal and interest accrued in the Trust Account in accordance with Colombier’s organizational document and IPO prospectus (i) to cover tax obligations of Colombier, (ii) to fund working capital requirements, in an amount of up to $1,000,000 per annum, and (iii) up to $100,000 to pay dissolution expenses.

“PIPE Investment” means any subscription agreements entered by Colombier with investors, between the execution of the Merger Agreement and the Closing, relating to a private equity investment in Colombier to purchase shares of Colombier in connection with a private placement, and/or enter into backstop arrangements with potential investors, in either case on terms mutually agreeable to PSQ and Colombier.

“Private Placement” means the private placement consummated simultaneously with the IPO in which Colombier issued the Private Warrants to the Sponsor.

5

“Private Warrants” means one (1) whole warrant entitling the holder thereof to purchase one (1) share of Colombier Class A Common Stock at a purchase price of $11.50 per share.

“Proposals” means the NTA Proposal, the Business Combination Proposal, the Charter Proposal, the Advisory Charter Proposals, the Incentive Plan Proposal, the ESPP Proposal, the NYSE Proposal and the Adjournment Proposal.

“Proposed Bylaws” means the amended and restated bylaws of the Combined Company in the form included as Annex C to this proxy statement/prospectus, to be adopted by Colombier upon consummation of the Business Combination.

“Proposed Charter” means the restated certificate of incorporation of Colombier in the form included as Annex B to this proxy statement/prospectus, to be adopted by Colombier pursuant to the Charter Proposal.

“PSQ” means PSQ Holdings, Inc., a Delaware corporation, prior to the Business Combination. References herein to PSQ will include its subsidiaries to the extent reasonably applicable.

“PSQ Board” means the board of directors of PSQ.

“PSQ Common Stock” means, collectively, the Common Stock, par value $0.001 per share, of PSQ prior to the Business Combination.

“PSQ Convertible Debt Conversion” means the mandatory conversion of all of the issued and outstanding PSQ Convertible Debt Notes for shares of PSQ Common Stock at the applicable conversion ratio as set forth in the PSQ Convertible Debt Notes.

“PSQ Convertible Debt Notes” means up to $15.0 million of 5% mandatorily convertible notes issued or issuable by PSQ in connection with the Permitted Financing and which will convert into shares of PSQ Common Stock immediately prior to completion of the Business Combination.

“PSQ Convertible Securities” means, collectively, each outstanding option, warrant, convertible note or other right to subscribe or purchase any capital stock of PSQ or securities convertible into or exchangeable for, or that otherwise confer on the holder any right to acquire any capital stock of PSQ.

“PSQ Founder” means Michael Seifert, the current Chief Executive Officer of PSQ.

“PSQ Stockholder Support Agreements” means the Company Stockholder Support Agreements entered into simultaneously with the execution of the Merger Agreement by Colombier, PSQ and holders of capital stock of PSQ sufficient to approve the Merger and other Transactions (including any required separate class votes), as may be amended, modified or supplemented.

“PSQ Stockholders” refers to holders of PSQ Common Stock immediately prior to the Effective Time.

“Public Shares” means Colombier Class A Common Stock underlying the Units sold in the IPO, including any overallotment securities acquired by Colombier’s underwriters.

“Public Stockholders” means holders of Public Shares.

“Public Warrant” means one (1) whole redeemable warrant that was included in as part of each Unit, entitling the holder thereof to purchase one (1) share of Colombier Class A Common Stock at a purchase price of $11.50 per share.

“Purchaser Representative” means the Sponsor, in its capacity as Purchaser Representative from and after the Closing in accordance with the terms of the Merger Agreement.

“Record Date” means the close of business on [•], 2023, the date on which only holders of record of the Colombier Common Stock are entitled to notice of the Colombier Special Meeting and to vote at the Colombier Special Meeting and any adjournments or postponements of the Colombier Special Meeting.

“Redemption” means the right of the holders of Colombier Class A Common Stock to have their shares redeemed in accordance with the procedures set forth in this proxy statement/prospectus and the Current Charter.

“Redemption Price” means an amount equal to the price at which the Colombier Class A Common Stock is redeemed or converted pursuant to the Redemption.

6

“Reference Time” means 11:59 p.m. Pacific Time on the date prior to the Closing Date.

“Required Proposals” means the Business Combination Proposal, the Charter Proposal, the Incentive Plan Proposal, the ESPP Proposal and the NYSE Proposal.

“SEC” means the U.S. Securities and Exchange Commission.

“Securities Act” means the Securities Act of 1933, as amended.

“Sponsor” means Colombier Sponsor LLC, a Delaware limited liability company.

“Target Companies” means PSQ and each of its direct and indirect subsidiaries.

“Transaction Expenses” means the aggregate unpaid fees and expenses of Colombier and PSQ immediately prior to the Closing incurred in connection with or related to the authorization, preparation, negotiation, execution or performance of the Merger Agreement, any Ancillary Agreements related thereto and all other matters related to the consummation of the Merger Agreement.

“Transactions” means the Business Combination, including the Merger and all of the transactions contemplated by the Merger Agreement and the Ancillary Agreements.

“Trust Account” means the trust account of Colombier, established at the time of the IPO, containing the net proceeds of the sale of the Units in the IPO, including from overallotment securities sold by Colombier’s underwriters, and the sale of Private Warrants following the closing of the IPO.

“Trust Agreement” means the Investment Management Trust Agreement, dated as of June 8, 2021, by Colombier and the Trustee, as well as any other agreements entered into related to or governing the Trust Account.

“Trustee” means Continental Stock Transfer & Trust Company, a New York corporation, in its capacity as Trustee under the Trust Agreement.

“UHY” means UHY LLP, PSQ’s independent registered public accounting firm.

“Underwriting Agreement” means that certain underwriting agreement, dated as of June 8, 2021 by and between Colombier and the IPO Underwriter.

“Units” means the units issued in the IPO (including overallotment units acquired by the IPO Underwriter) consisting of one (1) share of Colombier Class A Common Stock and one-third (1/3) of one Public Warrant.

“Warrants” means Private Warrants and Public Warrants, collectively.

Share Calculations and Ownership Percentages

Unless otherwise specified (including in the sections entitled “Unaudited Pro Forma Condensed Combined Financial Information” and “Beneficial Ownership of Securities”), the share calculations and ownership percentages set forth in this proxy statement/prospectus with respect to the Combined Company’s stockholders following the Business Combination are for illustrative purposes only and assume the following (certain capitalized terms below are defined elsewhere in this proxy statement/prospectus):

1. That, prior to the completion of the Merger, the PSQ Convertible Debt Conversion occurs in accordance with the terms of the Merger Agreement.

2. That, immediately prior to the Effective Time, PSQ Convertible Debt Notes in an aggregate principal amount of $14.25 million convert into 128,317.611975 shares of PSQ Common Stock (which excludes additional shares of PSQ Common Stock issuable, simultaneous with such conversion, as a result of accrued interest on the PSQ Convertible Debt Notes in an amount to be determined based on the Closing Date of the Business Combination).

3. That none of the PSQ Stockholders exercise appraisal rights in connection with the Merger.

4. That other than pursuant to the PSQ Convertible Debt Conversion, PSQ does not issue any additional equity or equity-linked securities prior to the Closing.

7

5. That no Public Stockholders exercise their redemption rights prior to (in the event that, in connection with a meeting of Colombier stockholders convened prior to the Closing Date, if any, Public Stockholders are provided an opportunity to redeem Public Shares in accordance with the terms of the Current Charter) or in connection with the Closing of the Business Combination. Please see the section entitled “The Colombier Special Meeting — Redemption Rights.”

6. That there are no transfers or forfeitures of securities held by the Sponsor on or prior to the Closing Date.

7. That no holders of Warrants exercise any of the outstanding Warrants.

8. That there are no issuances of equity securities by Colombier prior to the Closing.

9. That, at the Closing, consistent with the terms of the Merger Agreement, 165,000 shares of PSQ Common Stock, representing all of the shares of PSQ Common Stock held by the PSQ Founder, are cancelled in consideration for the issuance by Colombier to the PSQ Founder in the Merger of 3,207,646 shares of Class C Common Stock of the Combined Company.

10. That PSQ’s Closing Net Indebtedness will be equal to $0.

The share calculations and ownership percentages set forth in this proxy statement/prospectus with respect to the Combined Company’s stockholders following the Business Combination also do not include any shares reserved for issuance in connection with, or equity awards that may be made in connection with or following completion of the Business Combination pursuant to, the Incentive Plan or ESPP, in each case, contemplated to be adopted in connection with the completion of the Business Combination, and do not give effect to any potential future issuances of Earnout Shares.

8

CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTS

Certain statements contained in this proxy statement/prospectus may constitute “forward-looking statements” within the meaning of the “safe harbor” provisions of the United States Private Securities Litigation Reform Act of 1995. This includes, without limitation, statements regarding the financial position, business strategy and the plans and objectives of management for future operations, including as they relate to the potential Business Combination, of Colombier. These statements constitute projections, forecasts and forward-looking statements, and are not guarantees of performance. Such statements can be identified by the fact that they do not relate strictly to historical or current facts. When used in this proxy statement/prospectus, forward-looking statements may be identified by the use of words such as “estimate,” “continue,” “could,” “may,” “might,” “possible,” “predict,” “should,” “would,” “plan,” “project,” “forecast,” “intend,” “will,” “expect,” “anticipate,” “believe,” “seek,” “target,” “designed to” or other similar expressions that predict or indicate future events or trends or that are not statements of historical facts. In addition, any statements that refer to projections, forecasts or other characterizations of future events or circumstances, including any underlying assumptions, are forward-looking statements.

Colombier and PSQ caution readers of this proxy statement/prospectus that these forward-looking statements are subject to risks and uncertainties, most of which are difficult to predict and many of which are beyond Colombier’s and PSQ’s control, which could cause the actual results to differ materially from the expected results. These forward-looking statements include, but are not limited to, statements regarding estimates and forecasts of financial and performance metrics, projections of market opportunity and market share, potential benefits and the commercial attractiveness to its customers of products and services sold through PSQ’s platform, the potential success of PSQ’s marketing and expansion strategies, potential benefits of the Business Combination (including with respect to stockholder value), and expectations related to the terms and timing of the Business Combination. These statements are based on various assumptions, whether or not identified in this proxy statement/prospectus, and on the current expectations of PSQ’s and Colombier’s management and are not predictions of actual performance. These forward-looking statements are provided for illustrative purposes only and are not intended to serve as, and must not be relied on by any investor as, a guarantee, an assurance, a prediction or a definitive statement of fact or probability. Actual events and circumstances are difficult or impossible to predict and will differ from assumptions. These forward-looking statements are subject to a number of risks and uncertainties, including:

• changes in the competitive industries and markets in which PSQ operates or plans to operate;

• changes in applicable laws or regulations affecting PSQ’s business;

• the ability of PSQ to implement business plans, forecasts, and other expectations after the completion of the Business Combination, and identify and realize additional opportunities;

• risks related to PSQ’s limited operating history, the rollout and/or expansion of its business and the timing of expected business milestones;

• risks related to PSQ’s potential inability to achieve or maintain profitability and generate significant revenue;

• current and future conditions in the global economy, including as a result of economic uncertainty, and its impact on PSQ, its business and the markets in which it operates;

• the ability of PSQ to retain existing advertisers and consumer and business members and attract new advertisers and consumer and business members;

• the potential inability of PSQ to manage growth effectively;

• the ability to recruit, train and retain qualified personnel;

• estimates for the prospects and financial performance of PSQ’s business may prove to be incorrect or materially different from actual results;

• the inability of the parties to successfully or timely consummate the proposed Business Combination, including the risk that required regulatory approvals are not obtained, are delayed or are subject to unanticipated conditions that could adversely affect the Combined Company or the expected benefits of the proposed Business Combination or that the approval of the stockholders of Colombier or PSQ is not obtained;

9

• failure to realize the anticipated benefits of the proposed Business Combination;

• costs related to the Business Combination and the failure to realize anticipated benefits of the Business Combination or to realize estimated pro forma results and underlying assumptions, including with respect to estimated stockholder redemptions;

• risks related to future market adoption of PSQ’s offerings;

• risks related to PSQ’s marketing and growth strategies;

• the effects of competition on PSQ’s business;

• the amount of redemption requests made by Colombier’s public stockholders;

• the ability of Colombier or the Combined Company to issue equity or equity-linked securities in connection with the proposed Business Combination or in the future;

• PSQ and Colombier’s inability to complete the proposed Business Combination as contemplated by the Merger Agreement;

• matters discovered by the parties as they complete their respective due diligence investigation of the other;

• the inability to recognize the anticipated benefits of the proposed Business Combination, which may be affected by, among other things, the amount of cash available following any redemptions by Colombier stockholders;

• the ability of the Combined Company to meet the initial listing standards of the New York Stock Exchange upon consummation of the Business Combination;

• costs related to the proposed Business Combination;

• expectations with respect to future operating and financial performance and growth, including when PSQ will generate positive cash flow from operations;

• PSQ’s ability to raise funding on reasonable terms as necessary to develop its products in the timeframe contemplated by its business plan;

• PSQ’s ability to execute its anticipated business plans and strategy;

• the failure to satisfy the conditions to the consummation of the Business Combination, including the approval of the Business Combination and definitive agreements for the Business Combination by the stockholders of Colombier;

• the occurrence of any event, change or other circumstance that could give rise to the termination of the Business Combination;

• the outcome of any legal proceedings that may be instituted against PSQ or Colombier related to the Business Combination, and those factors discussed in Colombier’s IPO Prospectus under the heading “Risk Factors,” and other documents of Colombier filed, or to be filed, with the SEC; and

• other risks and uncertainties described in this proxy statement/prospectus, including those under the section entitled “Risk Factors.”